1

CENTRAL BANK AND ITS

ROLE IN FINANCIAL SYSTEM

______________________

1

Marijana Ćurak - University of Split, Faculty of Economics

Undergraduate study program: Business study

Financial institutions and markets

Academic year 2014/2015

10/21/2014

These lecture slides are based on the

book:

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

2

AGENDA

Introduction

Independence of central banks

Central bank’s balance sheet

Conduct of monetary policy: tools, goals, strategy, and

tactics

Review points

Marijana Ćurak - University of Split, Faculty of Economics

3

10/21/2014

2

INTRODUCTION (1)

Central banks are among the most

important players in financial markets

throughout the world

The banks are the government authorities

in charge of monetary policy

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

4

INTRODUCTION (2)

Monetary policy involves the management of

interest rates and the quantity of money

Central banks’ actions affect

interest rates

the amount of credit

and the supply of money

all of which have direct impacts not only on

financial markets, but also on aggregate output

and inflation

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

5

INDEPENDENCE OF CENTRAL BANKS (1)

An increasing number of nations have been giving more

independence to their central banks

Politicians who strongly oppose a central bank policy

often want to bring it under their supervision so as to

impose a policy more to their liking

Should the central bank be independent, or would we be

better of with a central bank under the control of the

president or the parliament?

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

6

3

THE CASE FOR INDEPENDENCE (1)

1. The strongest argument for an independent central

bank rests on the view that subjecting the central banks

to be more political pressures would impart an

inflationary bias to monetary policy

Politicians may be shortsighted because they are driven

by the need to win their next election

They are unlikely to focus on long-run objectives, such

as promoting stabile price level

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

7

THE CASE FOR INDEPENDENCE (2)

2. The political process in democratic societies

could lead to a political business cycle, in which

just before an election, expansionary policies are

pursued to lower unemployment and interest

rates

After the election, the bad effects of these

policies – high inflation and high interest rates –

cause problems

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

8

THE CASE FOR INDEPENDENCE (3)

3. Dangerous in case in which the central bank

can be used to facilitate financing of large

budget deficits by its purchases of government

securities

Government pressure on the central bank to

“help out” might lead to more inflation in the

economy

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

9

4

THE CASE FOR INDEPENDENCE (4)

4. Control of monetary policy is too

important to leave to politicians, a group

that has repeatedly demonstrated a lack

of expertise at making hard decisions on

issues of great economic importance, such

as reducing the budget deficit or

reforming the banking system

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

10

THE CASE AGAINST INDEPENDENCE (1)

1. It is undemocratic to have monetary policy

(which affects almost everyone in the economy)

controlled by an elite group that is responsible

to no one

2. To achieve a cohesive program that will

promote economic stability, monetary policy

must be coordinated with fiscal policy

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

11

THE CASE AGAINST INDEPENDENCE (2)

3. An independent central bank has not

always used its freedom successfully (the

FED failed in its stated role as lender of

last resort during the Great Depression)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

12

5

INDEPENDENCE OF CENTRAL BANKS (2)

There is yet no consensus on whether

central bank independence is a good

thing, although public support for

independence of the central bank seems

to have been growing

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

13

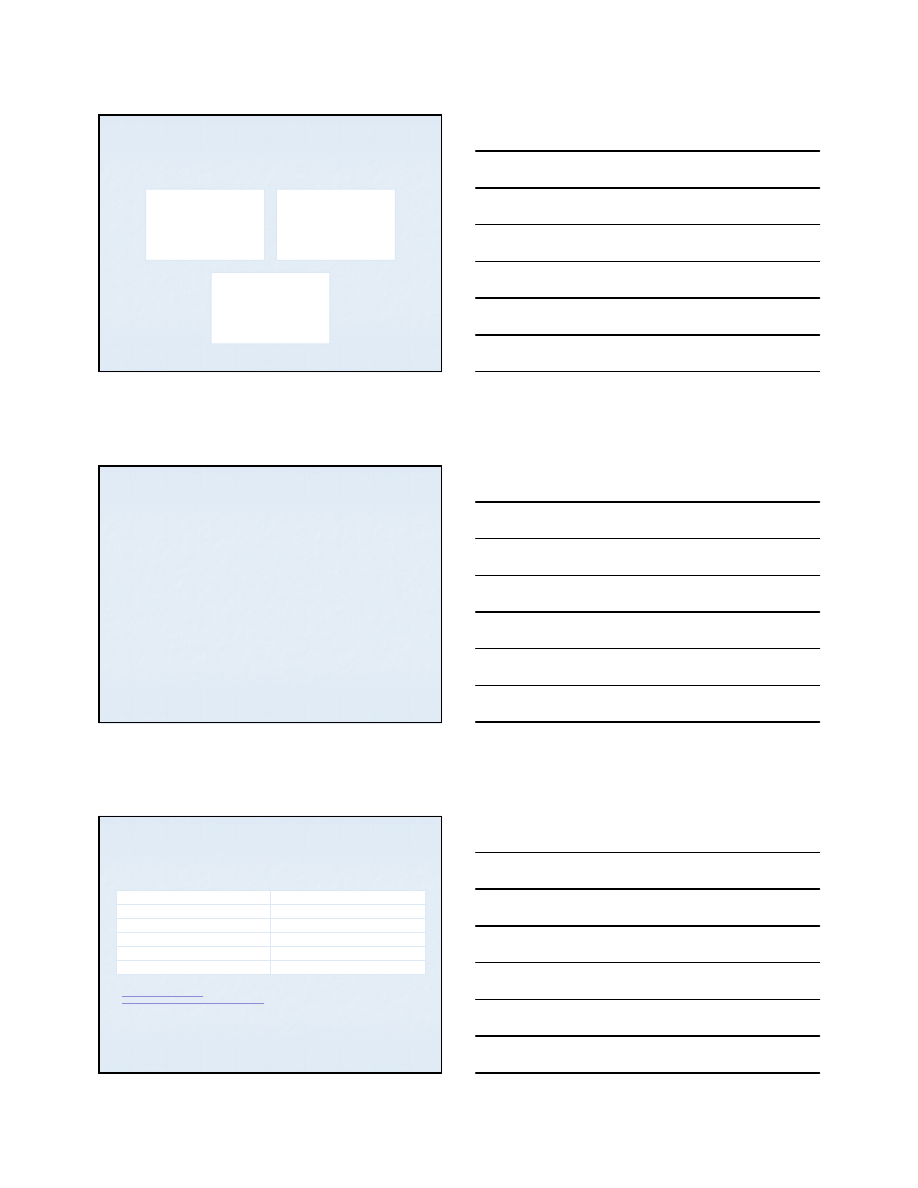

CENTRAL BANK BALANCE SHEET (1)

The conduct of monetary policy involves

actions that affect the central bank

balance sheet

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

14

CENTRAL BANK BALANCE SHEET (2)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

15

ASSETS

LIABILITIES

Government securities

Discount loans

Currency in circulation

Reserves

6

LIABILITIES (1)

Currency in circulation

The amount of currency in the hands of the

public (outside of banks) – an important

component of the money supply

Reserves

Deposits at the central bank plus currency

that is physically held by banks

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

16

LIABILITIES (2)

Reserves are assets for the banks but

liabilities for the central banks

Total reserves:

Required reserves – reserves that the central

bank requires banks to hold

Excess reserves: any additional reserves the

banks choose to hold

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

17

LIABILITIES (3)

The liabilities are an important part of the

money supply

The sum of the central bank’s monetary

liabilities (currency in circulation and

reserves) and the Treasury's monetary

liabilities is the monetary base

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

18

7

ASSETS

Government securites

The assets that covers the central bank’s

holdings of securites by the Treasury

Discount loans

Loans that are provided by the central bank

to banks

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

19

TOOLS OF MONETARY POLICY

Open market operations

Discount policy

Reserve requirements

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

20

OPEN MARKET OPERATIONS (1)

The central bank’s purchase or sale of

bonds in the open market

The most important monetary policy tool

because they are the primary determinant

of changes of reserves in the banking

system and interest rates

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

21

8

EXAMPLE OF OPEN MARKET OPERATION (1)

The central bynk purchase 100 EUR of

bonds from the publilc

The person/corporation that sels the 100

EUR bonds to the central bank deposit the

central bank money in the local bank

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

22

NONBANK PUBLIC

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

23

ASSETS

LIABILITIES

Securities

- 100

Deposits

+ 100

EXAMPLE OF OPEN MARKET OPERATION (2)

When the bank receives the money, it

evidence it on the depositor’s account with

100 EUR and then deposits it in its

account with the central bank, thereby

adding to its reserves

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

24

9

BANKING SYSTEM

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

25

ASSETS

LIABILITIES

Reserves

+ 100

Deposits

+ 100

EXAMPLE OF OPEN MARKET

OPERATION (3)

The central bank has gained 100 EUR of

securities, while reserves have increased

by 100 EUR

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

26

CENTRAL BANK

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

27

ASSETS

LIABILITIES

Securities

+ 100 Reserves

+ 100

10

OPEN MARKET OPERATIONS (2)

An open market purchase leads to an expansion

of reserves and deposits in the banking system

and hence to an expansion of the money supply

An open market sale leads to a contraction of

reserves and deposits in the banking system and

hence to a decline in the money supply

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

28

OPEN MARKET OPERATIONS (3)

There are to basic types of transactions:

Repurchase agreement (repo) – the central bank

purchases securities with an agreement that the seller

will repurchase them in a short period of time,

anywhere from 1 to 15 days from the original date of

purchase

Matched sale-purchase transaction (reverse repo) –

the central bank sells securities and the buyer agrees

to sell them to the central bank in the near future

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

29

DISCOUNT LENDING (1)

The central bank’s loan a bank

The discount window – the facility at which

banks can borrow reserves from the central

bank

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

30

11

EXAMPLE OF DISCOUNT LENDING

The central bank makes 100 EUR discount

loan to the Bank A

The central bank credits 100 EUR to the

bank’s reserve account

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

31

BANKING SYSTEM

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

32

ASSETS

LIABILITIES

Reserves

+ 100

Discount loans

+ 100

CENTRAL BANK

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

33

ASSETS

LIABILITIES

Discount loans

+ 100

Reserves

+ 100

12

DISCOUNT LENDING (2)

A discount loan leads to an expansion of

reserves, which can be lent out as

deposits, thereby leading to an expansion

of the money supply

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

34

DISCOUNT LENDING (3)

When a bank repays its discount loan and

so reduces the total amount of discount

lending, the amount of reserves decreases

along with the money supply

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

35

DISCOUNT LENDING (4)

Lender of last resort

In addition to its use as a tool to influence

reserves the money supply, discounting is

important in preventing and coping with

financial panics

The central bank prevent bank failures

spinning out of control

The central bank provides reserves to bank

when no one else would, preventing bank and

financial panics

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

36

13

TYPES OF DISCOUNT LOANS

Primary credit

Secondary credit

Seasonal credit

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

37

PRIMARY CREDIT

Standing lending facility

It allows healthy banks to borrow at very short

maturities

It is intended to be a backup source of liquidity for

sound banks

The interest rate on these loans is the discount rate

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

38

DISCOUNT RATES

Country/Central bank

Percentage

Japan

0.1

USA

0.5

ECB

0.75

UK

0.5

Poland

2.0

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

39

Souce: http://www.cbrates.com

and

http://mecometer.com/topic/central-bank-discount-rate/

(Assessed: October 18, 2014)

14

SECONDARY CREDIT

Is given to banks that are in financial

trouble and are experiencing severe

liquidity problems

The interest rate on these loans is set at a

higher, penalty rate to reflect the less-

sound condition of these borrowers

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

40

SEASONAL CREDIT

It is given to meet the need of a limited

number of small banks in vacation and

agricultural areas that have a seasonal

pattern of deposits

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

41

RESERVE REQUIREMENTS (1)

The regulations make it obligatory for

depository institutions to keep a certain

fraction of their deposits as reserves with

the central banks

Changes in reserves requirements affect

the demand for reserves

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

42

15

RESERVE REQUIREMENTS (2)

A rise in reserve requirements means that

banks must hold more reserves, and a

reduction means that they are required to

hold less

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

43

GOALS OF MONETARY POLICY (1)

The most important goal of monetary policy is

price stability – low and stabile inflation

Price stability is desirable because a rising price

level (inflation) creates uncertainty in the

economy, and that uncertainty might hamper

economic growth

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

44

GOALS OF MONETARY POLICY (2)

Other goals:

High employment

Economic growth

Stability of financial markets

Interest-rate stability

Stability in foreign exchange markets

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

45

16

INFLATION TARGETING (1)

It has become the most common

monetary policy strategy that countries

use to achieve price stability

Inflation targeting involves several

elements:

Public announcement of medium-term

numerical targets of inflation

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

46

INFLATION TARGETING (2)

An institutional commitment to price stability

as the primary, long-run goal of monetary

policy and a commitment to achieve the

inflation goal

An information-inclusive approach in which

many variables are used in making decisions

about monetary policy

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

47

INFLATION TARGETING (3)

Increased transparency of the monetary

policy strategy through communication with

the public and the markets about the plans

and objectives of monetary policy makers

Increased accountability of the central bank

for attaining its inflation objectives

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

48

17

TACTICS: CHOOSING THE POLICY INSTRUMENT (1)

The policy instrument (operating instrument) is

a variable that responds to the central bank’s

tool and indicates the stance (easy or tight) of

monetary policy

There are two basic types of policy instruments

Reserve aggregates (total reserves, non-borrowed

reserves, the monetary base, and the non-borrowed

base)

Interest rates (central bank funds rate and other

short-term interest rate)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

49

TACTICS: CHOOSING THE POLICY INSTRUMENT (1)

Central banks in small countries can choose

another policy instrument, the exchange rate

The policy instrument might be linked to an

intermediate target, such as a monetary

aggregate like M2 or a long-term interest rate

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

50

TACTICS: CHOOSING THE POLICY INSTRUMENT (3)

Intermediate targets stand between the

policy instrument and the goals of

monetary policy (e.g. price stability,

output growth)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

51

18

CRITERIA FOR CHOOSING THE POLICY

INSTRUMENT

Observability and measurability

Controllability

Predictable effect on goals

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

52

REVIEW POINTS (1)

Central banks are the government

authorities in charge of monetary policy

Tools of monetary policy:

Open market operations

Discount policy

Reserve requirements

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

53

REVIEW POINTS (2)

The price stability is the main goal of

monetary policy

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

54

19

REFERENCES

Mishkin F. S., Eakins, S. G. (2012), Financial

Markets + Institutions, Addison Wesley

Marijana Ćurak - University of Split, Faculty of Economics

55

10/21/2014

Wyszukiwarka

Podobne podstrony:

Angielski tematy Performance appraisal and its role in business 1

KAK, S 2000 Astronomy and its role in vedic culture

Aggression in music therapy and its role in creativity with reference to personality disorder 2011 A

Societys Problems and my role in helping it

Consent and Its Place in SM Sex

Keynesian?onomic Theory and its?monstration in the New D

Kiermasz, Zuzanna Investigating the attitudes towards learning a third language and its culture in

Software Vaccine Technique and Its Application in Early Virus Finding and Tracing

Peter d Stachura Antisemitism and Its Opponents in Modern Poland Glaukopis, 2005

MRS and its application in Alzheimer s disease

Masonry and its Symbols in the Light of Thinking and Destiny by Harold Waldwin Percival

Should the Marine Corps Expand Its Role in Special Operations

Tea polyphenols and their role in cancer prevention and chemotherapy

Thorax morphology and its importance in establishing relationships within Psylloidea Hemiptera Stern

MONEY AND BANKING NBP – THE CENTRAL BANK IN POLAND

THOMPSON shamanism in the RV and its central asia antecedents

więcej podobnych podstron