EBIT/EPS Analysis

The tax benefit of debt

Trade-off theory

Practical considerations in the

determination of capital structure

CAPITAL STRUCTURE

Lecture 2

Kevin Campbell, University of Stirling, October 2006

2

2

Capital structure

Issues:

EBIT-EPS analysis

The tax shield benefit of debt

The trade-off theory of capital structure

Practical considerations that affect the

capital structure decision

Kevin Campbell, University of Stirling, October 2006

3

3

Business Risk vs Financial

Risk

Business risk is the variability of a

firm’s Earnings Before Interest and

Taxes (EBIT)

Financial risk arises from the use of

debt, which imposes a fixed cost in

the form of interest payments =

financial leverage

.

Kevin Campbell, University of Stirling, October 2006

4

4

EBIT/EPS analysis

Examines how different capital

structures affect earnings available to

shareholders (EPS) and risk

Question: for different levels of

EBIT

,

how does financial leverage affect

EPS

?

Kevin Campbell, University of Stirling, October 2006

5

5

Risk and the Income

Statement

Sales

Business – Variable costs

Risk – Fixed costs

EBIT

– Interest expense

Financial Earnings before taxes

Risk – Taxes

Net Income

EPS

= Net Income / no. of shares

Kevin Campbell, University of Stirling, October 2006

6

6

Current and Proposed Capital

Structures

CURRENT

PROPOSED

Total assets

$100 million $100 million

Debt

0 million

50 million

Equity

100 million

50 million

Share price

$25

$25

No. of shares

4,000,000 2,000,000

Interest rate

10%

10%

Note: for the purpose of simplicity we ignore taxes in this

example

Kevin Campbell, University of Stirling, October 2006

7

7

CURRENT CAPITAL STRUCTURE

No Debt, 4 Million Shares (millions

omitted)

EBIT 50%

EBIT 50%

EBIT 50%

EBIT 50%

BELOW

BELOW

ABOVE

ABOVE

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EBIT

$6.00

$12.00 $18.00

– Int 0.00

0.00 0.00

NI

$6.00

$12.00 $18.00

EPS

$ 1.50

$ 3.00

$ 4.50

Kevin Campbell, University of Stirling, October 2006

8

8

EBIT 50%

EBIT 50%

EBIT 50%

EBIT 50%

BELOW

BELOW

ABOVE

ABOVE

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EBIT

$6.00

$12.00 $18.00

– Int 5.00

5.00 5.00

NI

$1.00

$ 7.00

$13.00

EPS

$ 0.50

$ 3.50

$ 6.50

PROPOSED CAPITAL STRUCTURE

50% Debt (10% Coupon), 2 million

Shares

(millions

omitted)

Kevin Campbell, University of Stirling, October 2006

9

9

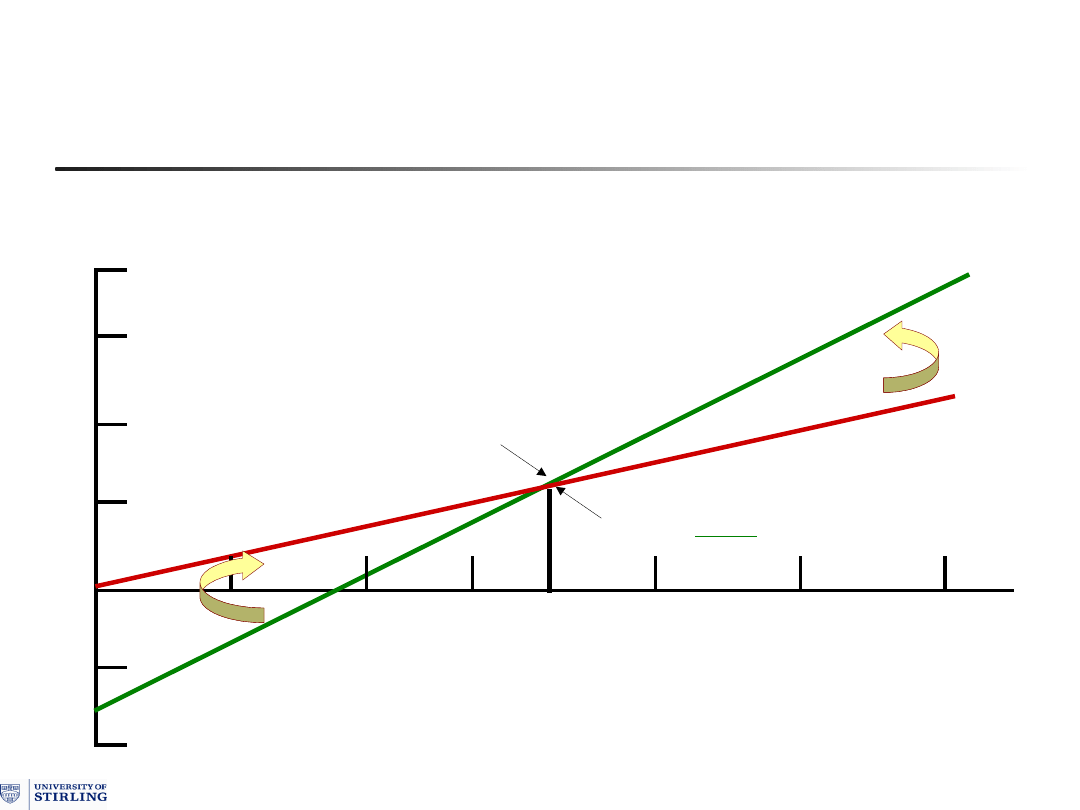

EBIT/EPS analysis

Current versus Proposed

Current

(no debt)

Proposed

(with

debt)

EPS

8

6

4

2

0

-2

-4

3

6

9 10

12

15

18

EBIT

For EBIT up to £10m,

equity financing is

best

For EBIT greater than

£10m, debt financing is

best

Kevin Campbell, University of Stirling, October 2006

10

10

The impact of financial

leverage

If EBIT is > 10, the levered capital

structure is preferable, ie EPS is higher

If EBIT is < 10, the unlevered capital

structure is preferable

Conclusion: whether or not debt is

beneficial is dependent upon the

capacity of firms to generate EBIT

Kevin Campbell, University of Stirling, October 2006

11

11

Indifference Level

The break-even EBIT occurs where the

lines cross

At that level of EBIT both capital

structures have the same EPS

Kevin Campbell, University of Stirling, October 2006

12

12

Set the two EPS values equal to each other

and solve for EBIT:

Current (unlevered) Proposed (levered)

(EBIT-Int)(1-T) = (EBIT-Int)(1-T)

S S

Since we assume T=0

(EBIT-Int)

=

(EBIT-Int)

S S

Breakeven Point

Kevin Campbell, University of Stirling, October 2006

13

13

Break-even EBIT

(millions

omitted)

10

$

20

$

2

)

5

($

4

4

2

2

)

1

.

50

($

4

EBIT

EBIT

EBIT

EBIT

EBIT

EBIT

EPS

EPS

L

U

Kevin Campbell, University of Stirling, October 2006

14

14

EPS

U

1.5 3.0 4.5

EPS

L

0.5 3.5 6.5

Spread

U

3.0

Spread

L

6.0 … that’s RISK

The impact of financial

leverage

EBIT 50%

EBIT 50%

EBIT 50%

EBIT 50%

BELOW

BELOW

ABOVE

ABOVE

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EXPECTED

EXPECTED

Kevin Campbell, University of Stirling, October 2006

15

15

The impact of financial

leverage

Leverage increases EPS if EBIT is high

enough.

At very low levels of EBIT, EPS can be

negative – as interest on debt has

priority over payments to shareholders.

Financial leverage produces a broader

spread of EPS values, ie shareholders’

returns are less predictable. This

represents added RISK.

Kevin Campbell, University of Stirling, October 2006

16

16

Summary: EBIT/EPS analysis

Indicates EBIT values when one capital

structure may be preferred over

another

Analysis of expected EBIT can focus on

the likelihood of actual EBIT exceeding

the indifference point

Kevin Campbell, University of Stirling, October 2006

17

17

Because interest on debt is

deducted from EBIT before the

amount of tax paid is calculated,

there is a benefit to debt … in the

form of lower corporate taxes

Consider an example …

The tax benefit of debt

Kevin Campbell, University of Stirling, October 2006

18

18

Firm

U

nlevered Firm

L

evered

No debt

$10,000 of 12% Debt

$20,000 Equity $10,000 in Equity

40% tax rate 40% tax rate

The tax benefit of debt

Both firms have same business risk and

EBIT of $3,000.

They differ only with respect to use of

debt.

U

has $20K in Equity &

L

has $10K in

Equity

Kevin Campbell, University of Stirling, October 2006

19

19

EBIT

$3,000

$3,000

Interest

0

1,200

EBT

$3,000

$1,800

Taxes (40%) 1 ,200 720

NI

$1,800

$1,080

ROE

9.0

%

10.8

%

Firm U Firm L

U; 1.8/20K =

9

% L; 1.08 / 10K =

10.8

%

The tax benefit of debt

Kevin Campbell, University of Stirling, October 2006

20

20

Why does financial leverage

increase the overall return to

investors?

Investors include both:

Debtholders (banks & bondholders)

Shareholders

Total return to investors:

U: NI = $1,800.

L: NI + Interest = $1,080 + $1,200 = $2,280.

Taxes paid:

U: $1,200

L: $720 Difference = $480

More EBIT goes to investors in Firm L

Kevin Campbell, University of Stirling, October 2006

21

21

Because the Government subsidizes debt,

and the tax savings go to the investors.

The tax savings are called the “

tax shield

”

and grows proportionally with the increase of

debt.

Why does financial leverage

increase the overall return to

investors?

Kevin Campbell, University of Stirling, October 2006

22

22

Debt versus Equity

Basic point. A firm’s

cost of debt

is always

less than its

cost of equity

.

Why?

debt has seniority over equity

debt has a fixed return

the interest paid on debt is tax-deductible.

It may appear a firm should use as much

debt and as little equity as possible due to

the cost difference … but this ignores the

potential problems associated with debt.

A Basic Capital Structure

Theory

Kevin Campbell, University of Stirling, October 2006

23

23

A Basic Capital Structure

Theory

There is a

trade-off

between the

benefits

of using debt and the

costs

of

using debt.

The use of debt creates a

tax shield

benefit

from the interest on debt.

The costs of using debt, besides the obvious

interest cost, are the additional

financial

distress costs

and

agency costs

arising from

the use of debt financing.

Kevin Campbell, University of Stirling, October 2006

24

24

The costs of

financial distress

associated with debt

Bankruptcy costs

including legal and

accounting fees and a likely decline in the

value of the firm’s assets

Financial distress may also cause

customers, suppliers, and management to

take actions harmful to firm value.

A Basic Capital Structure

Theory

Kevin Campbell, University of Stirling, October 2006

25

25

Agency costs

arise from conflicts between

shareholders and bondholders

When you lend money to a business, you are

allowing the shareholders to use that money in

the course of running that business.

Shareholders interests are different from your

interests, because

You (as lender) are interested in getting your

money back

Shareholders are interested in maximizing their

wealth

A Basic Capital Structure

Theory

Kevin Campbell, University of Stirling, October 2006

26

26

Agency costs

associated with debt:

Restrictive covenants meant to protect

creditors can reduce firm efficiency.

Monitoring costs may be expended to insure

the firm abides by the restrictive covenants.

As the level of debt financing increases, the

contractual and monitoring costs are

expected to increase.

A Basic Capital Structure

Theory

Kevin Campbell, University of Stirling, October 2006

27

27

Capital structure:

practical considerations

In addition to the variables described by

the trade-off theory of capital structure, a

variety of practical considerations also

affect a firm’s capital structure decisions:

Industry standards

Creditor and rating agency requirements

Maintaining excess borrowing capacity

Profitability and the need for funds

Managerial risk aversion

Corporate control

Kevin Campbell, University of Stirling, October 2006

28

28

Industry standards

It is natural to compare a firm’s capital

structure to other firms in the same

industry.

Business risk is a significant factor

impacting a firm’s capital structure and is

heavily influenced by a firm’s industry.

Evidence indicate firms’ capital structures

tend toward an industry average.

Practical considerations

Kevin Campbell, University of Stirling, October 2006

29

29

Creditor and Rating Agency Requirements

Firms need to abide by restrictive covenants,

which may include restrictions on the amount

of future debt.

Firms typically desire to appear financially

strong to potential creditors in order to

maintain borrowing capacity and low interest

rates.

Using less debt in capital structure helps to

maintain this appearance.

Practical considerations

Kevin Campbell, University of Stirling, October 2006

30

30

Maintaining Excess Borrowing

Capacity

Successful firms typically maintain

excess borrowing capacity.

This provides financial flexibility to react

to investment opportunities.

The maintenance of excess borrowing

capacity causes firms to use less debt

in their capital structure than otherwise.

Practical considerations

Kevin Campbell, University of Stirling, October 2006

31

31

Profitability and the Need for Funds

Profits can be paid out as dividends to

shareholders or reinvested in the firm.

If a firm generates high profits and

reinvests a large proportion back into

the firm, then it has a continuous

source of internal funding.

This will reduce the use of debt in the

firm’s capital structure.

Practical considerations

Kevin Campbell, University of Stirling, October 2006

32

32

Practical considerations

Managerial Risk Aversion

Well-diversified shareholders are likely to

welcome the use of financial leverage.

Management wealth is typically much

more dependent upon the success of the

company acting as their employer.

To the extent management can act on their

own desires, the firm is likely to have less

debt in its capital structure than is desired

by shareholders.

Kevin Campbell, University of Stirling, October 2006

33

33

Practical considerations

Corporate Control

Controlling owners may desire to issue

debt instead of ordinary shares since debt

does not grant ownership rights.

Firms with little financial leverage are

often considered excellent takeover

targets.

Issuing more debt may help to avoid a

corporate takeover.

Kevin Campbell, University of Stirling, October 2006

34

34

Summary

EBIT/EPS analysis

may be used to help

determine whether it would be better to

finance a project with debt or equity.

Firms must trade-off the

tax advantage

to

debt financing against the effect of debt on

firm risk

.

Because of the

tradeoff

between the tax

advantage to debt financing and risk, each

firm has an

optimal

capital structure.

Kevin Campbell, University of Stirling, October 2006

35

35

KONIEC

DZIĘKUJĘ ZA UWAGĘ

Kevin Campbell, University of Stirling, October 2006

36

36

Homework…

EBIT/EPS Analysis

A company is considering the following two capital structures:

Plan A:

sell 1,200,000 shares at £10 per share (£12 million total)

Plan B:

issue £3.5 million in debt (9% coupon) and sell 850,000

shares at £10 per share (£12 million total)

Assume a corporate tax rate of 50%

REQUIRED:

(a) What is the break-even value of EBIT?

(b) At this break-even value, what is the income statement for each

capital structure plan and the EPS?

(c) Draw a diagram to illustrate the trade-off between EBIT and EPS

Document Outline

- Slide 1

- Slide 2

- Slide 3

- Slide 4

- Slide 5

- Slide 6

- Slide 7

- Slide 8

- Slide 9

- Slide 10

- Slide 11

- Slide 12

- Slide 13

- Slide 14

- Slide 15

- Slide 16

- Slide 17

- Slide 18

- Slide 19

- Slide 20

- Slide 21

- Slide 22

- Slide 23

- Slide 24

- Slide 25

- Slide 26

- Slide 27

- Slide 28

- Slide 29

- Slide 30

- Slide 31

- Slide 32

- Slide 33

- Slide 34

- Slide 35

- Slide 36

Wyszukiwarka

Podobne podstrony:

196 Capital structure Intro lecture 1id 18514 ppt

195 KC Cost of capital lecture kisk 2id 18506 ppt

196 Capital structure Intro lecture 1id 18514 ppt

195 KC Cost of capital lecture kiskid 18505 ppt

Aktualności w leczeniu ostrej fazy udaru niedokrwiennego mózgu Gdańsk 2006

15427 Instrumementation system design lecture 1id 16462 ppt

2006 07 2id 25538

capital structure problem list number 1

Capital Structure Policy

15427 Instrumementation system design lecture 1id 16462 ppt

Carmina Burana, Gdańsk 2006 łacińskie teksty

Designing the capital structure

A Cebenoyan Risk Management, capital structure and lending at banks Journal of banking & finance v

11 Resusc 2id 12604 ppt

1 GENEZA KOMERCYJNEGO RYNKU OCHRONY W POLSCE 2id 9262 ppt

więcej podobnych podstron