1

BANKING OPERATIONS AND

MANAGEMENT

______________________

1

Marijana Ćurak - University of Split, Faculty of Economics

Undergraduate study program: Business study

Financial institutions and markets

Academic year 2014/2015

10/21/2014

These lecture slides are based on the

books:

Heffernan, S. (2005): Modern Banking, John

Wiley & Sons

Mishkin F. S., Eakins, S. G. (2012): Financial

Markets + Institutions, Addison Wesley

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

2

AGENDA

Banking operations – Types of Banking

The bank balance sheet

Basic banking

The general principles of bank management

Measuring bank performance

Financial innovation

Review points

Marijana Ćurak - University of Split, Faculty of Economics

3

10/21/2014

2

BANKING OPERATIONS

They depend on types of banks:

Universal banks

Commercial banks

Investment banks

Financial conglomerates

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

4

UNIVERSAL BANKS (1)

Universal banks offer the full range of

banking services, together with non-banking

financial services, under one legal entity

The banks have direct links between banking

and commerce through cross-shareholdings

and shared directorships

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

5

FINANCIAL ACTIVITIES OF UNIVERSAL BANKS (1)

Intermediation and liquidity via deposits and loans;

a byproduct is the payments system

Trading of financial instruments (e.g., bond, equity,

currency) and associated derivatives

Proprietary trading, that is, trading on behalf of the

bank itself, using its own trading book

Stockbroking

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

6

3

FINANCIAL ACTIVITIES OF UNIVERSAL BANKS (2)

Corporate advisory services, including mergers

and acquisitions

Investment management

Bancassurance

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

7

UNIVERSAL BANKS (2)

Germany is the home of universal banking (the

German hausbank)

Though German banks may own commercial

concerns, the sum of a bank’s equity

investments (in excess of 10% of the

commercial firm’s capital) plus other fixed

investments may not exceed the bank’s total

capital

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

8

UNIVERSAL BANKING (3)

In addition to a German bank lending to

commercial firms, it will also exert

influence through the Supervisory Board

Most of the shareholder seats are held by

bank executives because the bank

normally has a large shareholding

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

9

4

COMMERCIAL AND INVESTMENT

BANKS (1)

These terms originated in the United States,

though they are used widely in other countries

Under Glass Steagall Act (1933) commercial

banks were not allowed to underwrite securities

with the exception of municipal bonds, US

government bonds and private placements

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

10

COMMERCIAL AND INVESTMENT

BANKS (2)

Investment banks were prohibited from

offering commercial banking services

The objectives of the Act were twofold:

to discourage collusion among firms in the

banking sector

to prevent another financial crisis of the sort

witnessed between 1930 and 1933

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

11

COMMERCIAL BANKS (1)

Financial institutions that accept deposits

and make loans

Provide payment mechanism

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

12

5

COMMERCIAL BANKS (2)

Commercial banks offer

wholesale and

retail banking services

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

13

WHOLESALE BANKING

Typically involves offering intermediary, liquidity

and payment services to large customers such

as big corporations and governments

They offer business current accounts, make

commercial loans, participate in syndicated

lending and are active in the interbank markets

to borrow/lend from/to other banks

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

14

RETAIL BANKING

It offers the same services to numerous

personal banking customers and small

businesses

Retail banking is largely intrabank: the

bank itself accepts deposits and makes

many small loans

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

15

6

INVESTMENT BANKS (1)

Underwriting

Mergers and acquisitions

Trading – equities, fixed income (bonds),

proprietary

Fund management

Consultancy

Global custody

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

16

INVESTMENT BANKS (2)

Nor do investment banks offer liquidity as a service in

the same way as a standard bank

They contribute to increased liquidity in the system by

arranging new forms of finance for a corporation, but

this is quite different from meeting the liquidity demands

of depositors

Indeed, the functions of the investment bank differ so

much from the traditional bank that the term ‘‘bank’’

may be a misnomer

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

17

FINANCIAL CONGLOMERATE

Firm that undertakes at least two of five

financial activities:

intermediary/payments

insurance

securities/corporate finance

fund management and

advising on or selling investment products to

retail customers

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

18

7

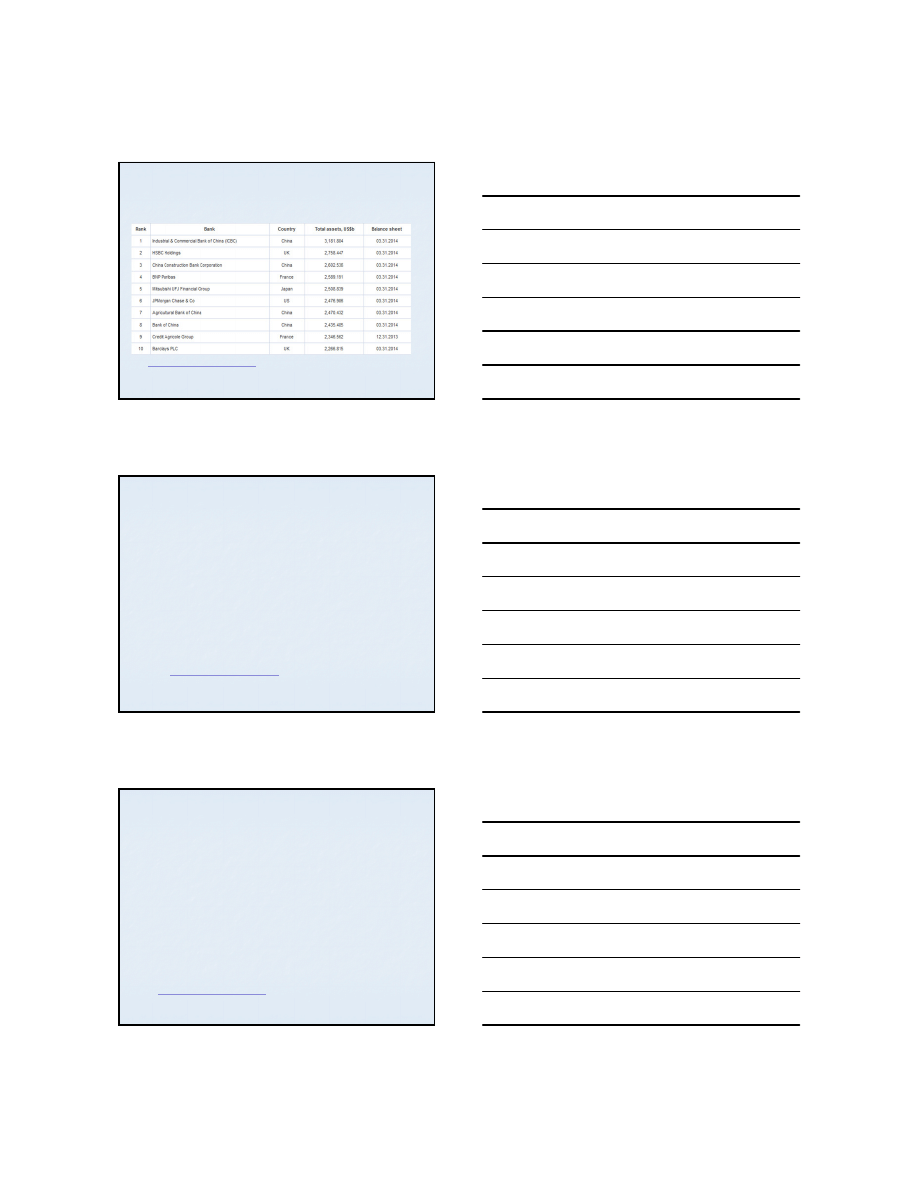

TOP BANKS IN THE WORLD IN 2014 (1)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

19

Source:

http://www.relbanks.com/worlds-top-banks/assets

(Accessed: October 18, 2014)

TOP BANKS IN THE WORLD IN 2014 (2)

For the third year in a row, Industrial &

Commercial Bank of China (ICBC) is the largest

bank in the World with assets of $3.182 trillion

Four of the top 10 banks are Chinese financial

institutions

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

20

Source:

http://www.relbanks.com/worlds-top-banks/assets

(Accessed: October 18, 2014)

TOP BANKS IN THE WORLD IN 2014 (3)

The Top 50 banks include:

10 Chinese banks

6 US banks

5 Japanese banks

5 French banks

5 UK banks

4 banks from Australia

3 from Canada and

3 from Germany

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

21

Source:

http://www.relbanks.com/worlds-top-banks/assets

(Accessed: October 18, 2014)

8

THE BANK BALANCE SHEET (1)

A bank’s balance sheet is list of its sources

of fund (liabilities) and uses to which the

funds are put (assets)

It has characteristics that:

Total assets = total liabilities + capital

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

22

THE BANK BALANCE SHEET (2)

Banks obtain funds by issuing liabilities such as

deposits, issuing of securities and by borrowing

They use the funds to acquire assets such as

loans and securities

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

23

LIABILITIES (1)

Demand deposits

Deposits that are payable on demand – if a depositor

shows up at the bank and request payment by

making a withdrawal, the bank must pay the

depositor immediately

They are usually the lowest cost source of bank funds

because depositors are willing to forgo some interest

to have access to a liquid asset

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

24

9

LIABILITIES (2)

Non-transaction deposits

Primary source of bank funds

The interest rates paid on these deposits are usually higher that

those on checkable deposits

Saving accounts

Funds that can be added or withdrawn at any time

Transactions and interest payments are recorded in a monthly

statement or in a passbook held by the owner of the account

Time deposit (certificates of deposit or CDs)

They have a fixed maturity length, ranging from several months to over

five years

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

25

LIABILITIES (3)

Borrowings

Borrowing from central bank, other banks and

corporations

Bank capital

Bank’s net worth

It equals the difference between total assets and

liabilities

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

26

ASSETS

Reserves

Required reserves

Excess reserves

Cash items in process of collection

Deposits at other banks

Securities

Loans

Other assets (the physical capital – bank

buildings, computers, and other equipment)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

27

10

BASIC BANKING (1)

Banks make profits by charging an interest

rate on their asset holdings of loans and

securities that is higher than the interest

and other expenses on their liabilities

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

28

BASIC BANKING (2)

Process of asset transformation – banks

make profits by selling liabilities with one

set of characteristics (a particular

combination of liquidity, risk, size, and

return) and using the proceeds to buy

assets with a different set of

characteristics

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

29

BASIC BANKING (3)

The bank “borrows short and lends long”

because it makes long-term loans and

funds them by issuing short-dated

deposits

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

30

11

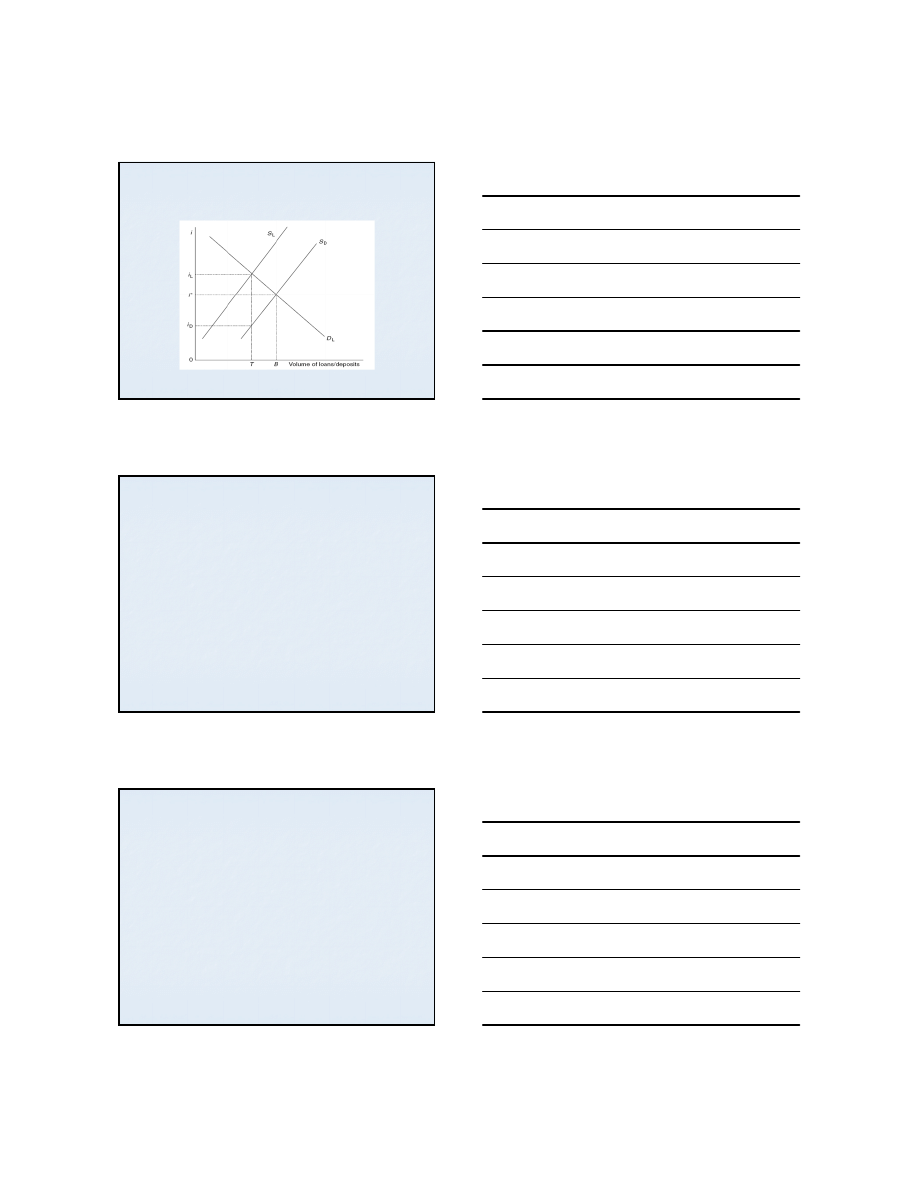

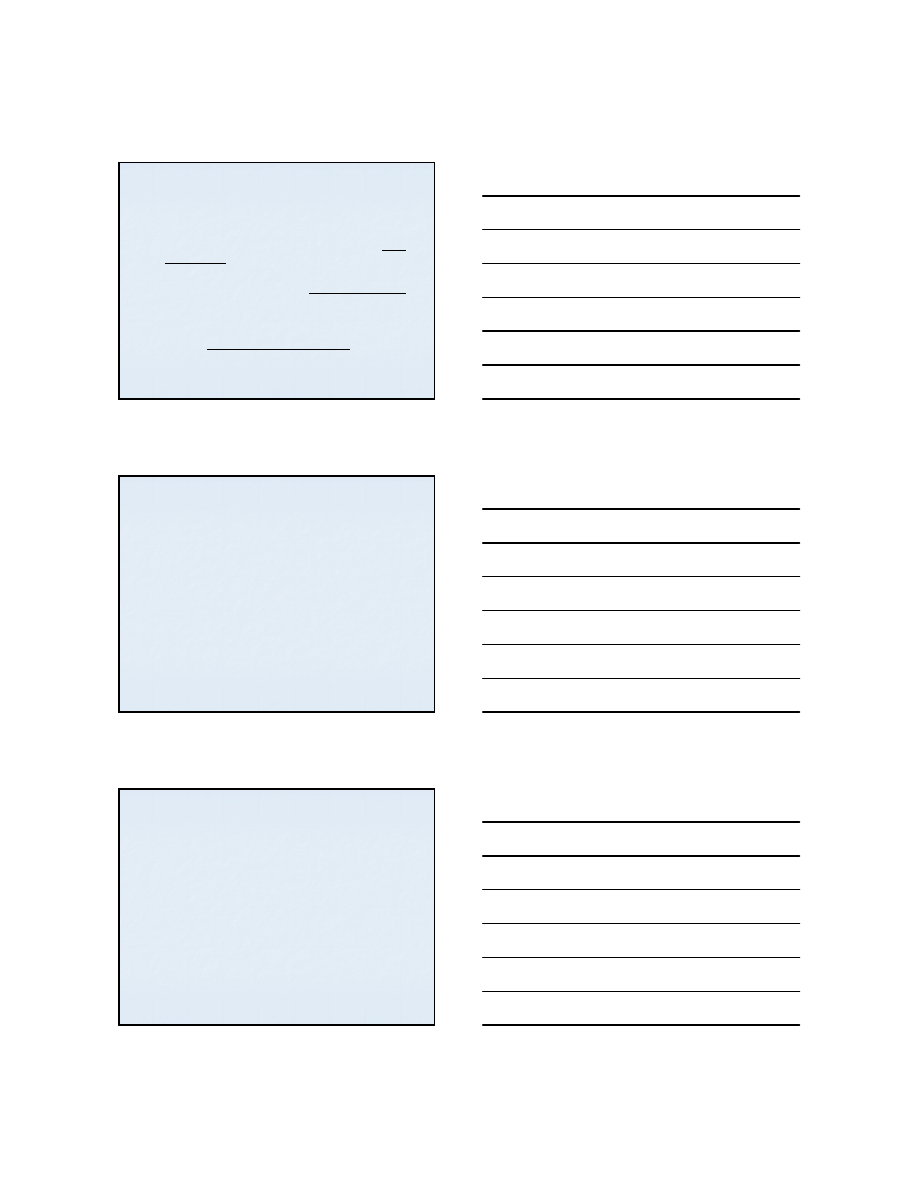

BANKING FIRM MODEL – INTERMEDIARY (1)

31

Source: Heffernan, 2005.

Marijana Ćurak - University of Split, Faculty of Economics

BANKING FIRM MODEL – INTERMEDIARY (2)

S

D

: supply of deposits curve

S

L

: supply of loans curve

D

L

: demand for loans curve

0T: volume of loans supplied by customers

i

∗

: market interest rate in the absence of the

intermediation costs

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

32

BANKING FIRM MODEL – INTERMEDIARY (3)

i

L

− i

D

: bank interest differential between the

loan rate (i

L

) and the deposit rate (i

D

) which

covers

the cost of the bank's intermediation

the cost of capital

the risk premium charged on loans

tax payments and

the institution’s profits

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

33

12

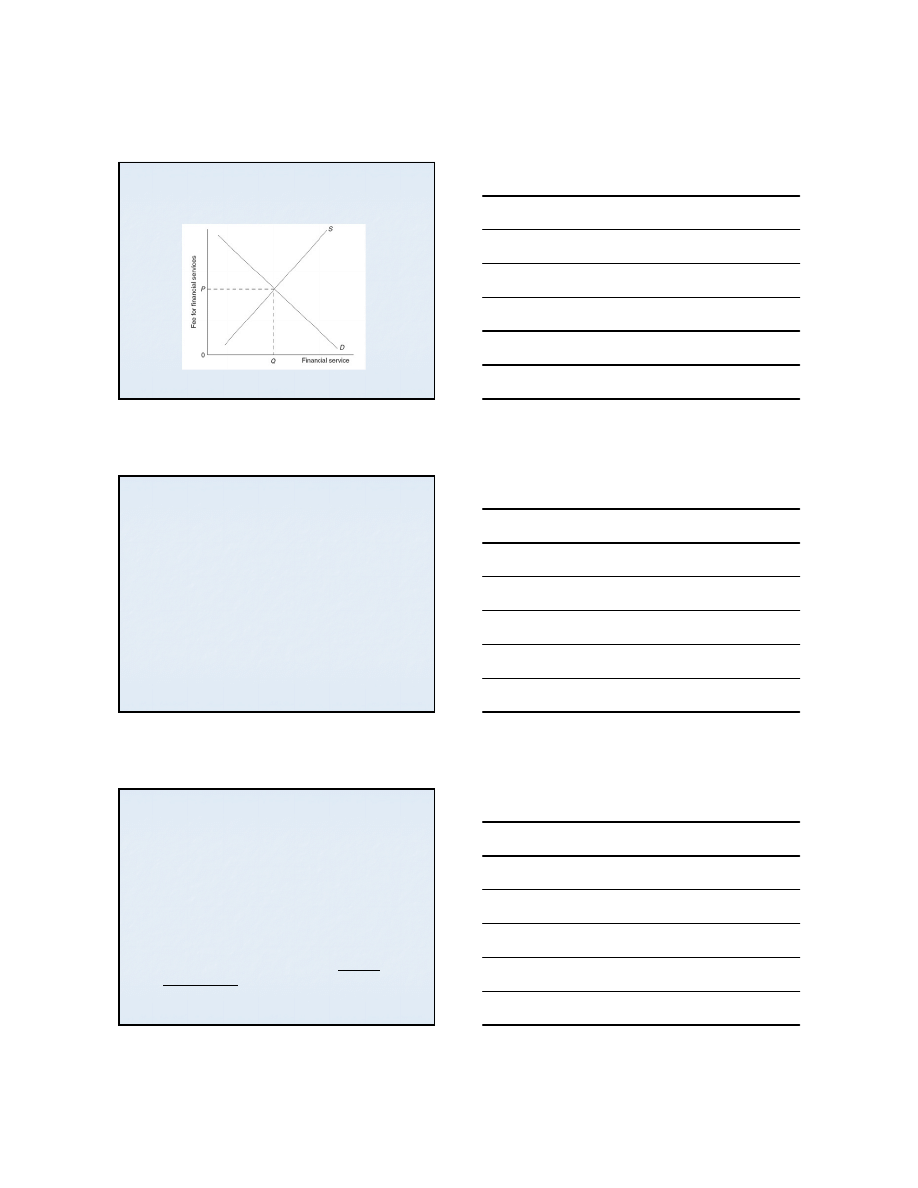

BANKING FIRM MODEL – FEE BASED

FINANCIAL PRODUCTS (1)

34

Izv. prof. dr. sc. Marijana Ćurak, Katedra za financije

Ekonomski fakultet, Sveučilište u Splitu

Source: Heffernan, 2005.

BANKING FIRM MODEL – FEE BASED

FINANCIAL PRODUCTS (2)

P: price for fee based services

Q: quantity demanded and supplied in

equilibrium

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

35

GENERAL PRINCIPLES OF BANK MANAGEMENT (1)

The bank manager has four main

concerns:

To make sure that the bank has enough ready

cash to pay its depositors when there are

deposit outflows (that is when deposits are

lost because depositors make withdrawals and

demand payment). To keep enough cash on

hand, the bank must engage in liquidity

management.

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

36

13

GENERAL PRINCIPLES OF BANK MANAGEMENT (2)

The bank manager has to take an acceptably low

level of risk by acquiring assets that have a low rate

of default and by diversifying asset holdings – asset

management

To acquire funds at low cost – liability management

The manager must decide the amount of capital the

bank should maintain and then acquire the needed

capital – capital adequacy management

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

37

LIQUIDITY MANAGEMENT (1)

Although more liquid assets tend to earn lower returns,

banks still desire to hold them

Banks hold excess and secondary reserves because they

provide insurance against the cost of a deposit outflow

The higher the costs associated with deposit outflows,

the more excess reserves banks will want to hold

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

38

LIQUIDITY MANAGEMENT (2)

When a deposit outflow occurs, holding excess

reserves allows the bank to escape the costs of:

Borrowing from other banks or corporations

Selling securities

Borrowing from the central bank

Calling in or selling off loans

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

39

14

ASSET MANAGEMENT (1)

Banks manage their assets to maximize

profits by seeking the highest returns

possible on loans and securities while at

the same time trying to lower risk and

making adequate provisions for liquidity

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

40

ASSET MANAGEMENT (2)

Banks try to find borrowers who will pay high

interest rates and unlikely to default on their

loans

They try to purchase securities with high returns

and low risk

They must attempt to lower risk by diversifying

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

41

ASSET MANAGEMENT (3)

Bank must manage the liquidity of its assets so

that it can satisfy its reserve requirements

without bearing huge costs

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

42

15

LIABILITY MANAGEMENT

Large banks actively seek out sources of funds

by issuing liabilities such as negotiable CDs or by

actively borrowing from other banks or

corporations

Importance of asset-liability management (ALM)

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

43

CAPITAL ADEQUACY MANAGEMENT (1)

Banks manage the amount of capital they hold

to

prevent bank failure (situation in which the bank

cannot satisfy its obligations to pay its depositors and

other creditors and so goes out of business)

meet bank capital requirements set by the regulatory

authorities

the amount of capital affects returns for the owners

(equity holders) of the bank

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

44

CAPITAL ADEQUACY MANAGEMENT (2)

They do not want to hold too much capital

because by so doing they will lower the returns

to equity holders

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

45

16

OFF BALANCE-SHEET ACTIVITIES (1)

The activities involve trading financial

instruments and generating income from fees

and loan sales, activities that affect bank profits

but do no appear on bank balance sheets

Off-balance-sheet activities have been growing

in importance for banks

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

46

OFF BALANCE-SHEET ACTIVITIES (2)

Generation of fee income

The fees that banks receive for providing specialized

services to their customers, such as making foreign

exchange trades on customer’s behalf, servicing a

mortgage-backed security by collecting interest and

principal payments and then paying them out

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

47

OFF BALANCE-SHEET ACTIVITIES (3)

Trading activities and risk management

techniques

In order to manage interest-rate risk banks trade in

derivatives market

Bank engaged in international banking also conduct

transitions in the foreign exchange market

All transactions in these markets are off-balance-

sheet activities because they do not have a direct

effect on the bank’s balance sheet

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

48

17

MEASURING BANK PERFORMANCES

Bank’s income statements

Operating income – the income that comes

form a bank’s ongoing operations

Operating expenses – the expenses incurred

in conducting the bank’s ongoing operations

Net operating income – Operating income –

operating expenses

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

49

MEASURES OF BANK PERFORMANCE (1)

Return on assets

Divides the net income of the bank by the

amount of its assets

It is a useful measure of how well a bank

manager is doing on the job because it

indicates how well a bank’s assets are being

used to generate profits

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

50

MEASURES OF BANK PERFORMANCE (2)

Return on equity (ROE)

Divides the net income of the bank by the

amount of its capital

It shows how much the bank is earning

bank’s owners equity investment

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

51

18

MEASURES OF BANK PERFORMANCE (2)

Net interest margin (NIM)

The difference between interest income and

interest expenses as a percentage of total

assets

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

52

FINANCIAL INNOVATION AND THE GROWTH OF

THE SHADOW BANKING SYSTEM

Shadow banking system – the system in which

bank lending has been replaced by lending via

the securities market

A change in the financial environment have

stimulated a search by financial institutions for

innovations that are likely to be profitable

The process of financial engineering

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

53

RESPONSE TO CHANGES IN DEMAND

CONDITIONS – INTEREST RATE VOLATILITY

Adjustable-rate mortgages

Mortgage loans on which the interest rate

changes when a market interest rate changes

Financial derivatives

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

54

19

RESPONSE TO CHANGES IN DEMAND

CONDITIONS – INFORMATION TECHNOLOGY

Bank credit and debit cards

Electronic banking

Electronic payment

E-money

Junk bonds

Commercial paper market

Securitization

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

55

REVIEW POINTS (1)

There are various bank operations

depending on type of banks:

Universal banks

Commercial banks

Investment banks

Financial conglomerates

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

56

REVIEW POINTS (2)

Fields of bank management:

Liquidity management

Asset management

Liability management

Capital adequacy management

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

57

20

REVIEW POINTS (3)

Banks response to changes in changes in

their business environment by various

innovations

10/21/2014

Marijana Ćurak - University of Split, Faculty of Economics

58

REFERENCES

Heffernan, S. (2005): Modern Banking, John

Wiley & Sons

Mishkin F. S., Eakins, S. G. (2012): Financial

Markets + Institutions, Addison Wesley

Marijana Ćurak - University of Split, Faculty of Economics

59

10/21/2014

Wyszukiwarka

Podobne podstrony:

Financial Institutions and Econ Nieznany

4 Steyr Operation and Maintenance Manual 8th edition Feb 08

lecture 15 Multivariate and mod Nieznany

Biogas Situation and Developmen Nieznany

Overview Of Gsm, Gprs, And Umts Nieznany

Meritum Bank wyrozniony za inno Nieznany

Bank korp id 79862 Nieznany (2)

Operation And Function Light Anti Armor Weapons M72 And M136 (2)

Barite Sag Measurement, Modeling, and Management

Operatorowe i czasowe rozwiazan Nieznany

[41]Hormesis and synergy pathways and mechanisms of quercetin in cancer prevention and management

Effects Of 20 H Rule And Shield Nieznany

132 Skirt drafting and sewing i Nieznany

placement test a b and answer k Nieznany

Diagnosis and Management of Hemochromatosis

Philosophical Analysis And Stru Nieznany

więcej podobnych podstron